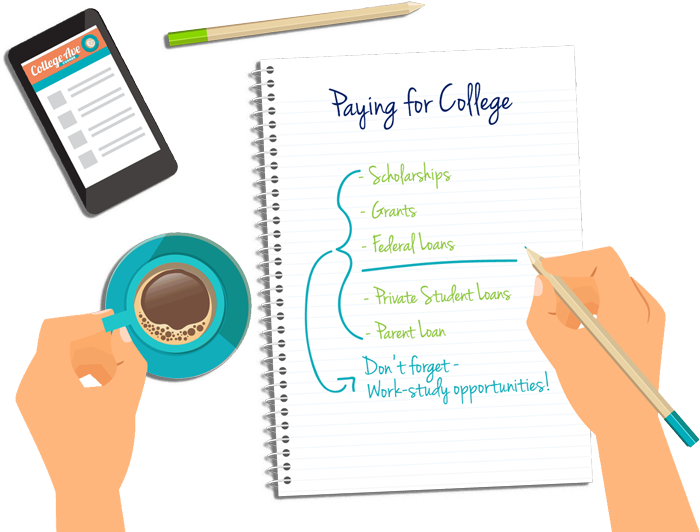

From the time you take out a student loan until you start paying it back, you’ll become a different person. Do future you a favor, financial experts say, and start thinking about the entire life cycle of your loan even before you sign on the dotted line and accept its terms.

There’s often a tendency to “hide from it a little bit – either in the preparation or repayment process,” says Angela Colatriano, Chief Marketing Officer of College Ave Student Loans. “It’s scary to think about sometimes, but it’s important to push through and make sure you're using all the tools and information available to you to make good choices up front.”

Having a sense of what a loan covers, what it will cost and when you have to start paying it back will set you up for success. Here, experts explain what undergraduates can expect from a private loan – including how to research, apply for and use it, and ultimately, the steps involved with repaying it. Bonus: Some special tips for graduate students and parents.